Iron & Steel

Iron & Steel

Power

Power

Plywood & Lamination

Plywood & Lamination

Sugar

Sugar

Tea

Tea

Oil & Gas

Oil & Gas

Solar & Wind

Solar & Wind

Agriculture

Agriculture

Chemical

Chemical

Food Product

Food Product

Real Estate &

Construction

Real Estate &

Construction

Logistics

Logistics

Automobile

Automobile

.jpg)

Blog

Read the following blogs to know about the recent trends in the industry and know about latest happenings.

Building from Bengal: Why Kolkata Is Our Advantage, Not Just Our Address

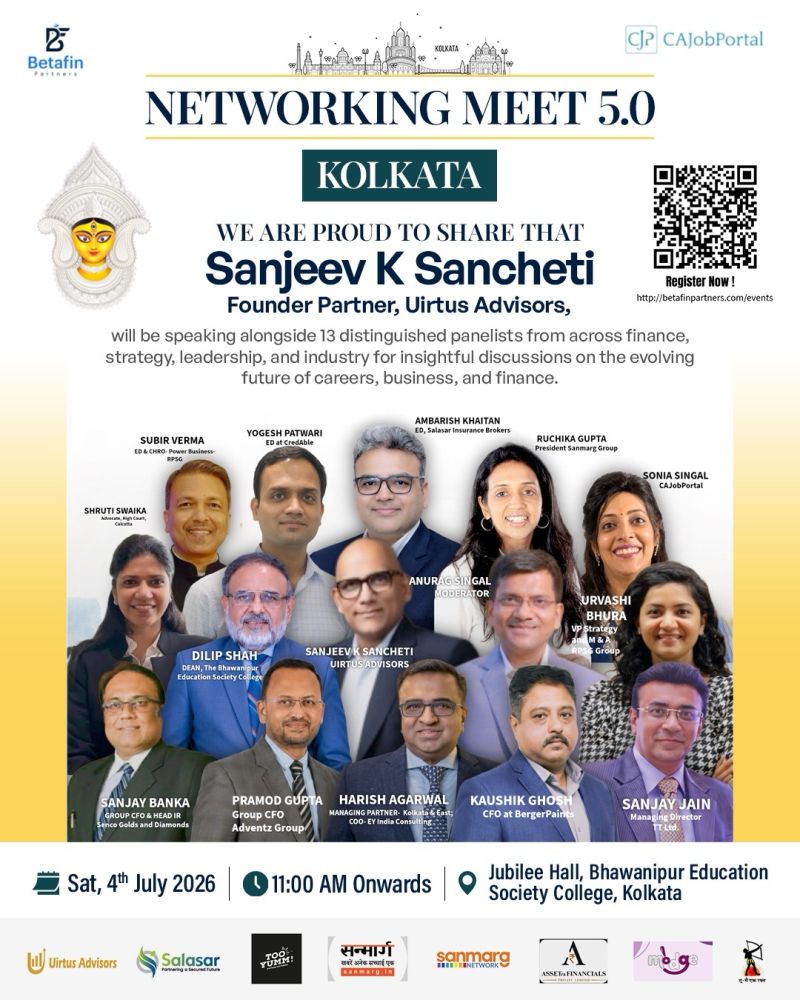

When people outside the region hear that one of East India's largest insurance broking firms is headquartered in Kolkata, the reaction is often a flicker of surprise. For much of the last two decades, conventional wisdom held that a financial-services business of national ambition had to be run from Mumbai or Delhi. At the 5th edition of the CAJobPortal × BetaFin Networking Event in Kolkata this July, that assumption was quietly, and convincingly, retired.

Our Executive Director, Mr. Ambarish Khaitan, joined the panel on "Resurgent Bengal: Careers, Choices & Regional Identity," moderated by Anurag Singal, alongside leaders from across the region's corporate landscape — Subir Verma, Urvashi Bhura, Shruti Swaika, Yogesh Patwari and Prof. Dilip Shah. Unlike the technical, execution-focused discussions elsewhere in the evening, this panel turned on a more personal question: what does it actually mean to build, stay, and grow where you are from? Or, as co-panelist Urvashi Bhura framed it, why your PIN code no longer decides how far a business can go.

The choice to stay

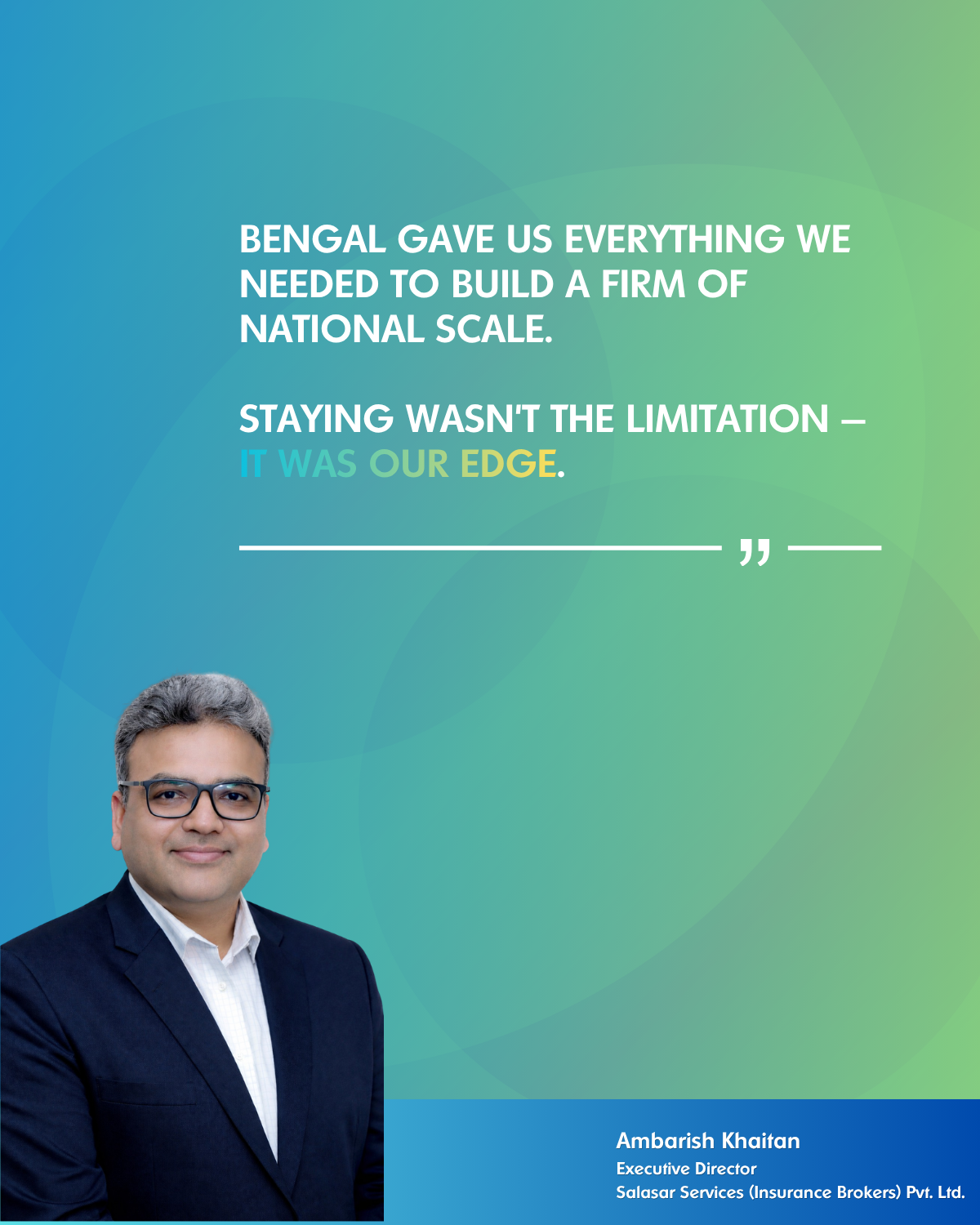

There is a version of the Salasar story that treats being based in Kolkata as a constraint to be overcome. We have never seen it that way. Being headquartered here meant that in the early years we walked into every boardroom — in Mumbai, in Delhi, anywhere — expecting to know the file better than anyone else in the room. Proximity was never going to win us the mandate, so substance had to. Over time, that discipline stopped being a compensation and became the edge itself. Bengal gave us everything we needed to build a firm of national scale; staying was not the limitation, it was our advantage.

That reframing matters beyond any single company. For a generation of professionals in the region, the default career narrative has been one of departure — that ambition and opportunity live elsewhere. The evening's discussion pushed hard against that idea, and the evidence is increasingly on its side. Bengal's financial ecosystem has spent three decades quietly reinventing itself, and today global-scale operations are being anchored from Kolkata across sectors, from manufacturing and consumer brands to infrastructure and finance.

Talent is the truest signal

If you want to know when a firm stops being seen as "regional," watch the direction talent moves. For years the story was one of out-migration: capable people leaving for larger hubs. The turning point for us came when senior professionals began choosing to move to Kolkata to build their careers rather than away from it. When that calibre of talent arrives — and stays — the market re-rates you. Winning mandates on capability rather than relationships, and attracting the people who can deliver them, is what genuinely signals arrival.

The talent question is also where the region still has work to do, and the panel was candid about it. Retaining and attracting senior professionals requires local enterprises to offer real scope, real ownership and real progression — not branch-office roles. The organisations that understand this are already reshaping how Kolkata is perceived as a career destination.

An underrated opportunity hiding in plain sight

Ask what remains most overlooked in Bengal today, and our answer is straightforward: risk itself. The state's economy is diversifying at pace — manufacturing, ports, renewables, agri-business — and much of that new activity is still uninsured or badly under-insured. That gap represents one of the most significant, and least contested, advisory and broking opportunities in the region. It is precisely the kind of space a firm built here, with deep local relationships and national capability, is positioned to build for. We intend to.

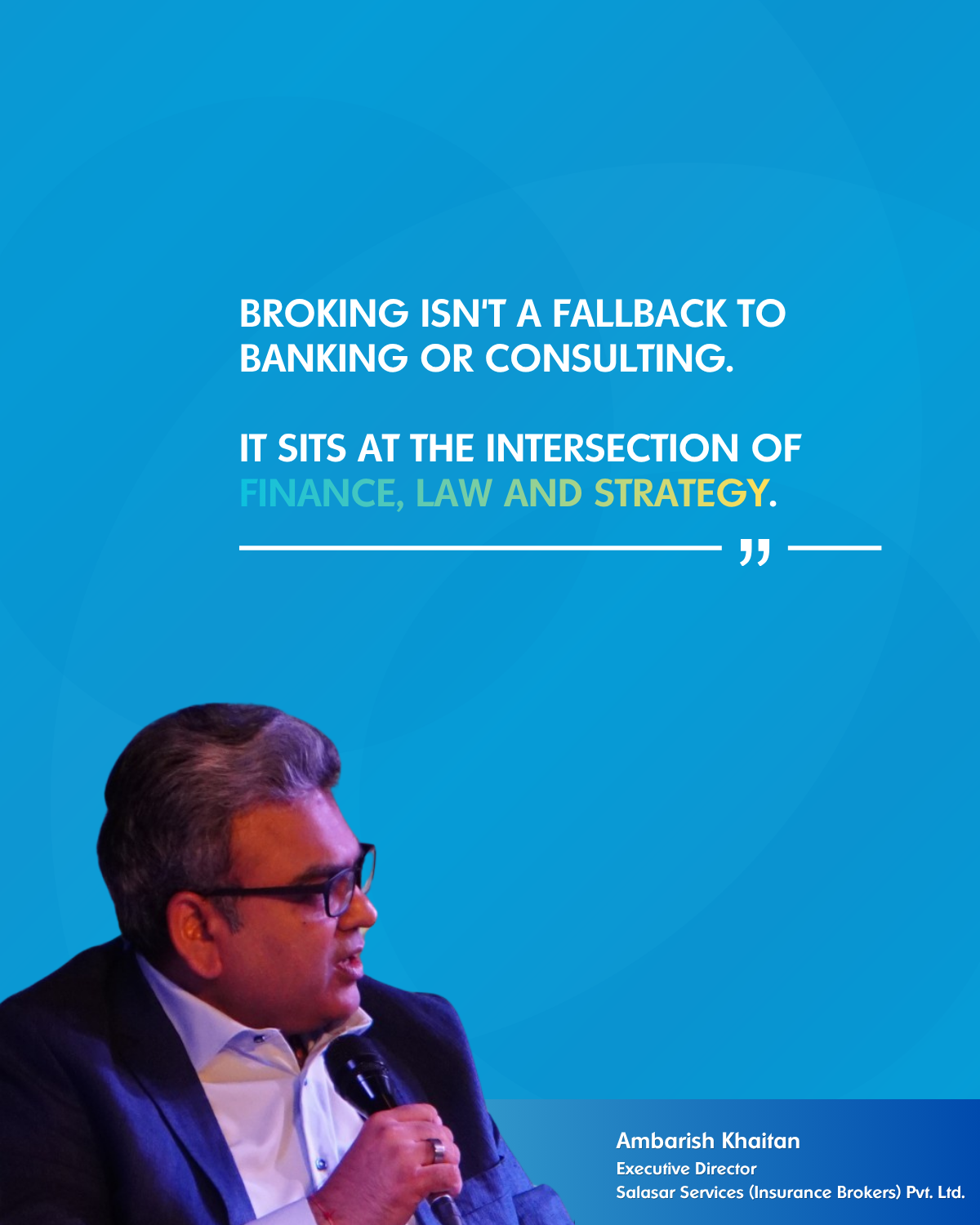

For the many chartered accountants and finance professionals in the room, this connects to a broader point about career choices. Insurance broking is too often treated as a fallback to banking or consulting. In reality it sits at the intersection of finance, law and strategy — advising CFOs and boards directly, reconstructing complex claims, and building expertise in specialised areas such as business interruption, cyber, parametric and trade-credit cover, where genuinely skilled brokers remain scarce relative to demand. For a young professional, that is not just a job; it is a chance to become one of the few people in the country who can do the work well.

A region writing its next chapter

What made the evening notable was not any single claim but the accumulated weight of many. Across two panels, senior leaders described the same shift from different vantage points: mindset, not geography, is now the binding constraint. Coverage in the Times of India the following day captured the theme plainly — finance leaders showcasing Bengal's rise and promise as a global hub.

For Salasar Services, this is more than a favourable narrative. It is the environment we have spent nearly two decades helping to build, and the one we are committed to for the decades ahead. Kolkata was never the compromise in our story. It was, and remains, the reason it worked.

👇 A few moments from the evening.

When people outside the region hear that one of East India's largest insurance broking firms is headquartered in Kolkata, the reaction is often a flicker of surprise. For much of the last two decades, conventional wisdom held that a financial-services business of national ambition had to be run from Mumbai or Delhi. At the 5th edition of the CAJobPortal × BetaFin Networking Event in Kolkata this July, that assumption was quietly, and convincingly, retired.

Our Executive Director, Mr. Ambarish Khaitan, joined the panel on "Resurgent Bengal: Careers, Choices & Regional Identity," moderated by Anurag Singal, alongside leaders from across the region's corporate landscape — Subir Verma, Urvashi Bhura, Shruti Swaika, Yogesh Patwari and Prof. Dilip Shah. Unlike the technical, execution-focused discussions elsewhere in the evening, this panel turned on a more personal question: what does it actually mean to build, stay, and grow where you are from? Or, as co-panelist Urvashi Bhura framed it, why your PIN code no longer decides how far a business can go.

The choice to stay

There is a version of the Salasar story that treats being based in Kolkata as a constraint to be overcome. We have never seen it that way. Being headquartered here meant that in the early years we walked into every boardroom — in Mumbai, in Delhi, anywhere — expecting to know the file better than anyone else in the room. Proximity was never going to win us the mandate, so substance had to. Over time, that discipline stopped being a compensation and became the edge itself. Bengal gave us everything we needed to build a firm of national scale; staying was not the limitation, it was our advantage.

That reframing matters beyond any single company. For a generation of professionals in the region, the default career narrative has been one of departure — that ambition and opportunity live elsewhere. The evening's discussion pushed hard against that idea, and the evidence is increasingly on its side. Bengal's financial ecosystem has spent three decades quietly reinventing itself, and today global-scale operations are being anchored from Kolkata across sectors, from manufacturing and consumer brands to infrastructure and finance.

Talent is the truest signal

If you want to know when a firm stops being seen as "regional," watch the direction talent moves. For years the story was one of out-migration: capable people leaving for larger hubs. The turning point for us came when senior professionals began choosing to move to Kolkata to build their careers rather than away from it. When that calibre of talent arrives — and stays — the market re-rates you. Winning mandates on capability rather than relationships, and attracting the people who can deliver them, is what genuinely signals arrival.

The talent question is also where the region still has work to do, and the panel was candid about it. Retaining and attracting senior professionals requires local enterprises to offer real scope, real ownership and real progression — not branch-office roles. The organisations that understand this are already reshaping how Kolkata is perceived as a career destination.

An underrated opportunity hiding in plain sight

Ask what remains most overlooked in Bengal today, and our answer is straightforward: risk itself. The state's economy is diversifying at pace — manufacturing, ports, renewables, agri-business — and much of that new activity is still uninsured or badly under-insured. That gap represents one of the most significant, and least contested, advisory and broking opportunities in the region. It is precisely the kind of space a firm built here, with deep local relationships and national capability, is positioned to build for. We intend to.

For the many chartered accountants and finance professionals in the room, this connects to a broader point about career choices. Insurance broking is too often treated as a fallback to banking or consulting. In reality it sits at the intersection of finance, law and strategy — advising CFOs and boards directly, reconstructing complex claims, and building expertise in specialised areas such as business interruption, cyber, parametric and trade-credit cover, where genuinely skilled brokers remain scarce relative to demand. For a young professional, that is not just a job; it is a chance to become one of the few people in the country who can do the work well.

A region writing its next chapter

What made the evening notable was not any single claim but the accumulated weight of many. Across two panels, senior leaders described the same shift from different vantage points: mindset, not geography, is now the binding constraint. Coverage in the Times of India the following day captured the theme plainly — finance leaders showcasing Bengal's rise and promise as a global hub.

For Salasar Services, this is more than a favourable narrative. It is the environment we have spent nearly two decades helping to build, and the one we are committed to for the decades ahead. Kolkata was never the compromise in our story. It was, and remains, the reason it worked.

👇 A few moments from the evening.

Salasar Services is one of India's leading insurance broking firms, advising businesses across the country on risk, insurance and claims from its base in Kolkata.

Zero GST, Wider Safety Net: How GST 2.0 Reforms Are Rewriting Life & Health Insurance in India

When India introduced the Goods and Services Tax (GST) in 2017, life insurance was mostly treated like any other taxable service. Term plans were charged a straight 18% GST on premiums, while savings-oriented and investment-linked products had complicated tax structures that confused both customers and advisors.ClearTax

With GST 2.0, that framing has changed dramatically. From 22 September 2025, GST on all individual life and health insurance policies has been reduced from 18% to 0%, as part of a wider overhaul of the GST system.Ministry of FinanceNDTV

Earlier analyses had already examined this shift at a policy level and explored what it could mean for the life insurance business and Indian households.Bimabazaar This updated piece builds on that work, brings in fresher data, and looks more closely at how GST 2.0 is already reshaping behaviour on the ground.

Disclaimer: This article is for general information only and should not be treated as tax, legal or investment advice. Please consult qualified professionals before making financial decisions.

1. Where We Started: GST and Life Insurance Before 2.0

Before GST 2.0, life insurance premiums fell under different effective GST rates depending on product type:

- Pure term insurance – 18% GST on the full risk premium, making the most protection-heavy products visibly more expensive for customers.PNB MetLife

- Traditional endowment and savings plans – the law applied 18% GST only on a specified portion of the premium, effectively working out to around 4.5% in the first year and 2.25% on renewals.ClearTax

- ULIPs and other investment-linked plans – different GST treatments across risk charges, fund management charges and allocation charges added layers of complexity for insurers and policyholders alike.PNB MetLife

From a household’s perspective, this meant:

- Term insurance – which offers the highest pure risk cover per rupee – looked disproportionately costly.

- Insurance often compared poorly with other instruments like mutual funds or small savings schemes, especially when customers focused on upfront costs rather than risk protection.

- It was hard to compare products because premiums, GST and charges were all structured differently.

At the same time, India remained structurally underinsured. Insurance penetration (total premiums as a percentage of GDP) was about 3.7% in FY24, with life insurance contributing only around 2.8% – below the global average near 7%.IBEFIRDAIBusiness Standard

Multiple studies estimate India’s mortality protection gap – the gap between the life cover people actually hold and what they genuinely need – at over 80%, translating to a shortfall in the range of USD 16.5–17 trillion in recent years.Aditya Birla CapitalET BFSINational Insurance AcademyPwC India

Against this backdrop, insurers, industry bodies and policymakers had already begun arguing that GST on protection products should be seen less as a revenue-generator and more as a barrier to building household resilience – exactly the context in which GST 2.0 was conceived.Bimabazaar

2. What GST 2.0 Has Changed for Life and Health Insurance

2.1 0% GST on Individual Life and Health Policies

The single most important change for individuals is straightforward:

All individual life insurance and health insurance policies now attract 0% GST on premiums. This marks a shift from the earlier 18% rate on term and many other covers.Ministry of FinanceSBI LifeNDTV

This 0% rate applies to:

- Pure term plans

- Traditional savings and endowment policies

- ULIPs and other investment-linked life products

- Individual and family health insurance policies

The benefit is focused on the retail customer. Many group insurance and non-life commercial lines continue to be taxed at 18%, so GST relief is being used as a targeted tool to strengthen personal financial security rather than to subsidise all forms of insurance across the board.SBI Life

2.2 Part of a Larger GST Overhaul

GST 2.0 is not just about insurance; it is a broader clean-up exercise. The earlier multi-slab structure has been compressed, leaving mainly 5% and 18% slabs, with a 40% rate reserved for a narrow basket of luxury and “sin” goods.Reuters

A wide list of essential or mass-consumption items – including some food, medicines and basic services – have also seen rate reductions. Government estimates suggest that the cumulative impact of these cuts, including the 0% GST on life and health premiums, could exert a modest downward pressure on inflation in the coming year.Reuters

Within this broader rationalisation, removing GST from individual life and health insurance sends a clear signal: the state now sees risk protection less as a taxable service and more as part of the country’s social and financial safety net.

3. What This Means for Households and Policyholders

3.1 Immediate Premium Savings (Illustrative Examples Only)

Note: The following examples are purely illustrative and the figures are for explanatory purposes only. Actual premiums and tax impacts will vary by insurer, age, cover amount, underwriting, product structure and other factors.

Under the old regime, if a family paid ₹20,000 a year for a term plan, the total outgo typically looked like this:

- Base premium: ₹20,000

- GST @18%: ₹3,600

- Total paid: ₹23,600

With GST now at 0% on individual life policies, the same policy with a ₹20,000 base premium simply costs ₹20,000 – an 18% saving on the tax portion alone.

For higher covers, the difference compounds. A young professional paying ₹50,000 annually for a large term cover would previously pay an additional ₹9,000 in GST, taking the total to ₹59,000. At 0% GST, the full ₹9,000 remains in the customer’s pocket. Over a 25-year policy term, that difference could add up to over ₹2.25 lakh before considering any investment returns on the saved amount.

Early indications from insurers and distributors suggest a visible uptick in interest, especially among first-time buyers and younger salaried customers who are now revisiting quotes that earlier looked slightly out of reach.SBI LifeNDTV

3.2 Narrowing India’s Protection Gap

India’s mortality protection gap is among the largest in the world. Various analyses have pegged this gap – the difference between required and actual life cover – at over 80%, translating into a multi-trillion dollar shortfall in household protection.Aditya Birla CapitalET BFSINational Insurance AcademyPwC India

Price has always been one of the big obstacles. When tax alone inflates the cost of a pure protection product by nearly one-fifth, many households either delay buying cover or settle for token sums assured (₹10–20 lakh) that would cover only a small fraction of their actual needs.

By taking GST on individual life and health premiums down to zero, the system effectively removes one major friction point. Over time, this should help:

- Lower the entry barrier for first-time buyers who were earlier put off by “add-on tax” at the payment stage.

- Encourage families who already have basic cover to step up their sum assured to more realistic income-replacement levels.

- Make protection more affordable for the growing middle class in Tier-2 and Tier-3 cities, where price sensitivity is high but aspirations are rising quickly.PwC India

All of this ties in with the Insurance Regulatory and Development Authority of India’s (IRDAI) long-term vision of “Insurance for All by 2047” – the goal that every Indian citizen and enterprise should have appropriate insurance cover by the time the country completes 100 years of independence.Drishti IASIRDAI

3.3 Trust, Transparency and Behaviour Change

For many consumers, it was always hard to justify why a product that protected their family’s future carried the same tax rate as many discretionary services.

By making individual life and health covers GST-free:

- The state is signalling that these products sit closer to sectors like healthcare and education – essential services that deserve policy support.

- Pricing becomes simpler and more transparent: what you see as the premium is what you actually pay, without last-minute tax surprises on the payment screen.

- Digital journeys become smoother, because the “extra” 18% that previously appeared at checkout and often caused drop-offs is no longer there.

Over time, this combination of lower cost and clearer communication can help shift life insurance from a product that is mostly “sold” to one that is increasingly “bought” by informed customers.

4. How GST 2.0 Affects Insurers and Intermediaries

4.1 Input Tax Credit and Cost Structures

While premiums on individual policies are now GST-free, insurers still pay GST on many of their inputs – including technology services, outsourcing arrangements and distribution commissions.ClearTax

Under the earlier regime, life insurers struggled to utilise input tax credit (ITC) fully, especially where exemptions existed in specific product lines. GST 2.0 relaxes some of these constraints and creates space for wider ITC usage, though the details – especially around commissions and reinsurance – are still evolving.Reuters

Industry bodies have pointed out a key pressure point: if GST on agents’ commissions continues at 18% while the underlying premiums become exempt, insurers may be left holding unrecoverable ITC, which can squeeze margins. There have been active calls to reduce GST on commissions to 0% as well, to align the full value chain.Times of India

4.2 Product Design and Innovation

High GST rates previously made it difficult to launch very low-ticket protection products or micro-insurance covers, because the tax cost could overwhelm thin margins.

With 0% GST on individual life and health premiums, insurers can:

- Design small-ticket policies for rural and semi-urban markets without worrying that GST will dominate the price point.National Insurance Academy

- Experiment with bundled offerings – for example, term covers paired with health riders or wellness programs – without layering on additional tax complexity.

- Put more emphasis on pure risk protection instead of leaning heavily on investment-heavy products just to protect margins.

Global research indicates that in a higher interest-rate environment, life insurance profitability can get a natural boost from better investment income. In India, the removal of GST on retail protection products adds another lever by reducing the tax drag on premiums.Reinsurance News

4.3 Compliance and Operational Simplicity

The earlier GST framework required insurers to slice and dice premiums – especially for ULIPs and traditional plans – into different components, each with its own GST treatment. That led to extra work in accounting, reconciliation and tax audits.ClearTaxPNB MetLife

With 0% GST on individual life and health policies, much of this complexity simply disappears. Insurers can devote more managerial bandwidth to underwriting quality, claims management and customer experience rather than to managing tax anomalies.

5. The Bigger Picture: Penetration, Inclusion and Public Finance

5.1 Insurance Penetration and Financial Inclusion

Despite strong growth in premiums over the past two decades, India’s overall insurance penetration still trails the global average, hovering around 3.7–4% compared to roughly 7% worldwide.IBEFIRDAIBusiness Standard

At the same time, research from the National Insurance Academy and others has highlighted that health, natural catastrophe and life protection gaps remain high – exceeding 90% in some segments – leaving households heavily exposed to medical expenses and income shocks.National Insurance AcademyPwC India

India has already taken several steps to reduce this vulnerability, from Ayushman Bharat and state health schemes to crop and catastrophe covers. Even so, out-of-pocket medical expenditure remains a significant burden for many families, especially in the lower and middle income brackets.Moneycontrol

By reducing GST on individual life and health premiums to zero, GST 2.0 becomes another tool in this broader inclusion toolbox – encouraging households to complement public schemes with their own private risk cover.

5.2 Revenue Trade-offs vs Long-Term Stability

Any tax cut has a short-term fiscal cost. Government and independent estimates suggest that exempting health and life insurance premiums from GST could cost the exchequer several thousand crore rupees per year in forgone revenue; one panel assessment placed this impact at close to ₹9,700 crore.Reuters

When combined with the wider GST 2.0 rate cuts on goods and other services, the total revenue impact of the overhaul has been estimated in the range of tens of thousands of crore, although still below some of the early worst-case projections.Reuters

However, these headline numbers only tell part of the story. If lower GST on protection products:

- Raises life and health insurance penetration meaningfully,

- Reduces the need for ad-hoc government relief packages after disasters or medical crises, and

- Strengthens long-term household savings and capital formation,

then the dynamic benefits – in terms of financial stability, reduced poverty risk and deeper capital markets – could easily outweigh the initial static revenue loss over time.

6. What Different Stakeholders Should Do Now

6.1 For Consumers

- Re-check your life and health covers. If you postponed buying adequate term or health insurance because premiums felt high, it is worth revisiting the numbers in the light of 0% GST.

- Upgrade under-sized policies. Many families hold symbolic covers that would replace only a fraction of their income. Use the tax saving to move closer to realistic protection levels.

- Lock in long-term protection early. Term premiums are driven by age and health; GST savings simply add another reason not to delay.

6.2 For Insurers and Intermediaries

- Clearly show the “before vs after”. Use marketing, policy documents and digital journeys to highlight how much GST 2.0 has reduced the overall cost of protection.SBI Life

- Double down on digital and vernacular outreach. The next barriers are awareness and access, not tax. Smooth, multilingual onboarding journeys can convert curiosity into cover.

- Design protection-first solutions. With the tax drag removed, it becomes more attractive to build term-heavy, micro-insurance and gig-worker products that purely focus on risk protection.Reinsurance News

6.3 For Policymakers and Regulators

- Align GST across the value chain. Revisiting GST on commissions and related services will help avoid ITC leakage and ensure that the 0% rate on premiums does not inadvertently compress margins in parts of the ecosystem.Times of India

- Invest in financial literacy. Targeted campaigns in smaller cities and towns can help people understand how much cover they actually need and how GST changes affect them.National Insurance Academy

- Track outcomes, not just revenue. Over the next 3–5 years, data on penetration, claims and protection gaps will show whether GST 2.0 is delivering on its goal of wider, deeper protection.

7. Conclusion: From Taxed Service to Social Shield

GST 2.0 has done more than tweak rates on a spreadsheet. By taking GST on individual life and health insurance premiums from 18% to 0%, it has fundamentally repositioned protection in India’s policy framework – from a taxable service to a public-good–adjacent safety net.Ministry of Finance

The reform makes genuine protection more affordable, simplifies a previously confusing tax landscape, supports IRDAI’s “Insurance for All by 2047” vision, and gives the industry space to innovate around pure risk solutions rather than just savings products.Drishti IASIRDAI

Whether GST 2.0 turns out to be the inflection point many hope for will depend on what happens next: how quickly insurers redesign products, how seriously intermediaries take their advisory role, and how actively households use this opportunity to close their own protection gaps.

For now, one thing is clear: India has taken a decisive step toward making financial protection a necessity rather than a luxury – and the removal of GST on life and health insurance premiums is right at the heart of that shift.

8. FAQs on GST 2.0 and Life Insurance

FAQ 1. What is GST 2.0 and how does it affect life insurance?

GST 2.0 is a comprehensive overhaul of India’s Goods and Services Tax structure that, among other changes, reduces GST on individual life and health insurance premiums from 18% to 0%. For policyholders, this means lower overall cost of protection and simpler, more transparent pricing.Ministry of FinanceSBI LifeNDTV

FAQ 2. From when does the 0% GST rate apply on life and health insurance?

The 0% GST rate applies to eligible individual life and health insurance premiums that fall due on or after 22 September 2025. Premiums paid before that date were subject to the older GST rates and are not typically eligible for refunds.Ministry of FinanceNDTV

FAQ 3. Does 0% GST apply to all kinds of insurance policies?

No. The 0% rate is focused on individual life and health insurance policies. Many group covers and other general insurance products, such as commercial lines, continue to attract GST – often at the standard 18% rate.Ministry of FinanceSBI LifeReuters

FAQ 4. Will my existing policy automatically become cheaper because of GST 2.0?

If your existing policy falls into the category of individual life or health insurance, future premiums that fall due on or after 22 September 2025 should reflect the 0% GST rate. However, past premiums paid under the old regime are unlikely to be refunded. The exact implementation can vary by insurer, so it is sensible to check your revised premium schedule.SBI LifeNDTV

FAQ 5. Does this mean I no longer need other forms of savings or investments?

No. Removing GST from life and health insurance makes protection more affordable, but it does not replace the role of savings and investments. A sound household financial plan should balance adequate protection with long-term wealth creation through appropriate investment instruments.Aditya Birla CapitalPwC India

Next-Gen InsurTech: How AI Agents Are Driving Hyper-Personalized Customer Engagement

India’s insurance landscape is entering a new era—one where AI agents do more than respond to queries. From anticipating policy gaps to delivering tailor-made coverages via WhatsApp and UPI, these smart assistants are redefining customer engagement, speeding up claims, and building deeper trust. Scroll down to see how seven key pillars are driving this transformation across InsurTech in India.

Sources & Further Reading

Cyber Insurance in India: Trends, Risks & Market Outlook

India’s rapid digital transformation—fueled by widespread internet access, growing fintech activity, and government-led initiatives such as Digital India—has widened the nation’s cyber threat surface. As industries adopt digital tools and services, vulnerabilities also multiply, making them lucrative targets for cybercriminals.

Cyberattacks like phishing, ransomware, data breaches, and DDoS incidents now frequently impact critical sectors such as BFSI, healthcare, retail, and even small businesses. Amid this escalating risk environment, cyber insurance has emerged as a strategic safeguard that helps organizations manage financial losses resulting from such events.

This article explores the relevance, structure, types, and evolving role of cyber insurance in India, while offering insight into how it contributes to building national cyber resilience and risk preparedness.

What is Cyber Security Insurance?

What does cyber security insurance mean?

Cyber security insurance, also known as cyber liability insurance, is a specialized policy that protects individuals and organizations from the financial impact of cyber incidents. It covers a range of losses stemming from events such as data breaches, ransomware attacks, system failures, and cyber extortion.

What does it typically cover?

Coverage often includes investigation of breaches, forensic audits, data restoration, legal expenses, regulatory fines, customer notification, credit monitoring, and even crisis communication and public relations efforts. Some policies extend to third-party liabilities and business interruption losses.

Major Causes of Cybersecurity Breaches

As cyber threats evolve, understanding the root causes of security breaches becomes essential for designing effective risk mitigation strategies and cyber insurance coverage. Businesses—both large and small—face increasing exposure to a variety of attack vectors that exploit human error, technological vulnerabilities, and insufficient security practices.

According to Security.org, a study of reported cyber incidents reveals that the majority of breaches stem from a combination of employee negligence, compromised credentials, and phishing attacks. Other contributors include ransomware, outdated software, and internal malicious activity. These vulnerabilities create a compelling case for organizations to adopt cyber insurance as a part of their overall risk management framework.

Types of Cyber Security Insurance and Its Relevance

Cyber threats are not one-size-fits-all, and neither are insurance solutions. Different policy types exist to address varying levels of exposure and risk—ranging from personal identity theft to corporate data breaches. Below are the major types of cyber insurance available in India and their relevance in today’s digital landscape:

- Individual Cyber Insurance: Designed for individuals, it covers risks such as identity theft, phishing scams, cyberstalking, financial fraud, and cyberbullying. With the increasing use of social media and digital banking, this form of coverage is becoming essential even for the average internet user.

- Business/Corporate Cyber Insurance: These are comprehensive policies tailored for organizations. They cover both first-party losses (like data restoration, business interruption, and cyber extortion) and third-party liabilities (legal claims resulting from customer data exposure).

- Data Breach Insurance: Specifically addresses the financial and operational impact of data exposure or theft. It typically includes costs for notifying affected customers, forensic investigations, legal representation, credit monitoring services, and public relations crisis management.

- Cyber Liability Insurance: Offers protection when third parties (e.g., customers, vendors) sue an organization for damages caused by a cyber incident. It covers court-ordered compensation, regulatory penalties, and legal settlements.

- Network Security Insurance: Covers losses from network compromise events like denial-of-service (DoS) attacks, malware infections, unauthorized access, and firewall breaches. It’s highly relevant for IT-driven businesses, banks, and e-commerce firms.

- Cybercrime Insurance: Protects against financial losses from crimes such as phishing, spoofing, cyber extortion, social engineering fraud, and ransomware attacks. This is particularly critical for fintechs and online retailers.

- Technology Errors & Omissions (Tech E&O) Insurance: Tailored for IT service providers, software developers, and consultants. It offers coverage against losses caused by professional negligence, coding errors, or implementation failures that lead to client damages.

Choosing the right type of cyber insurance policy depends on the entity's digital exposure, industry regulations, and nature of operations. For example, a healthcare firm might prioritize data breach insurance due to sensitive patient information, while a SaaS provider may lean towards Tech E&O coverage.

Need and Importance of Cyber Security Insurance in India

As India undergoes rapid digital transformation across sectors like banking, healthcare, education, and retail, the need for robust cyber security mechanisms has never been greater. Cyber insurance is no longer a luxury—it has become a necessity for both enterprises and individuals navigating the online ecosystem.

- Increasing Cyber Threats: India ranks among the top countries targeted by cyberattacks, witnessing a sharp rise in phishing, ransomware, identity theft, and data breach incidents [CERT-In].

- Protection Against Financial Loss: Cyber insurance helps mitigate the high costs associated with breaches, including revenue loss, regulatory fines, legal defense, and system recovery. This can run into crores for major companies.

- Support for SMEs: Small and medium-sized enterprises often lack the budget for advanced cyber defense systems. Insurance offers them a financial cushion against cyber risk, enabling business continuity.

- Compliance with Regulations: The Digital Personal Data Protection (DPDP) Act, 2023 and CERT-In guidelines mandate timely reporting and data protection standards. Cyber insurance policies help cover associated compliance costs.

- Crisis Management and Legal Aid: Policies often include access to legal counsel, PR crisis teams, and forensic experts, enabling insured organizations to respond swiftly and effectively to incidents.

- Reputation Management: Cyberattacks can severely damage brand trust. Many policies include reputation restoration services to manage media narratives and customer perception.

- Boosting the Digital Economy: By mitigating cyber risk, insurance encourages greater digital adoption across industries, fostering a more secure and resilient digital economy.

- Improving Cyber Hygiene: Insurers often require policyholders to implement minimum security measures such as firewalls, encryption, and regular audits—thereby uplifting cybersecurity standards across the board.

As cyber threats grow in complexity and scale, cyber insurance offers a strategic layer of defense that complements technical safeguards. It is a critical enabler of digital trust in India's evolving cyber ecosystem.

Global Cybersecurity & Fraud: A Broad Perspective

Cyber threats are no longer hypothetical; they have become a global economic crisis. Organizations across sectors face escalating risks—with massive financial repercussions and systemic vulnerabilities, particularly in cloud and IoT infrastructures.

- Cybercrime Costs: Global cybercrime damages are forecasted to exceed $10.5 trillion by 2025.[esentire]

- Ransomware Impact: Average recovery cost from ransomware attacks is around $4.54 million.[getastra]

- Phishing Attacks: Phishing and social engineering remain the most common breach methods, accounting for over 36% of all data breaches.[deepstrike]

- BEC (Business Email Compromise): Estimated global losses from BEC scams approached $3 billion in 2023.[fortra]

- Cloud & IoT Vulnerabilities: Over 60% of organizations experienced public cloud–related security incidents in 2024.[cybersecuritydistrict]

- Cybersecurity Talent Gap: The global shortfall of cybersecurity professionals is estimated at nearly 4 million unfilled positions in 2025.[weforum]

AI as an Influencer of Cyber Crime

Artificial Intelligence (AI), while revolutionary in defending against cyber threats, is also becoming a potent weapon in the hands of cybercriminals. By automating attacks and enhancing evasion techniques, AI has redefined the threat landscape, making cybercrime more scalable, adaptive, and unpredictable.

- AI-Driven Phishing & Deepfakes: Cybercriminals now use AI to craft hyper-personalized phishing emails and realistic deepfake videos or voice recordings, impersonating company executives or government officials to extract sensitive information or authorize fraudulent transactions. [Europol, 2024]

- Machine Learning for Password Cracking: ML algorithms are used to analyze massive datasets from past breaches, improving the speed and accuracy of brute-force password attacks. These models continuously learn from user behavior patterns, making them harder to detect and defend against. [Forbes Tech Council, 2024]

- AI-Powered DDoS Attacks: AI bots are increasingly orchestrating Distributed Denial-of-Service (DDoS) attacks that adapt in real-time to mitigation efforts. These bots analyze response patterns and dynamically change attack vectors, overwhelming targets with evolving tactics. [Imperva, 2023]

- Generative AI & Crime-as-a-Service: Tools like ChatGPT-clones and open-source generative models are being used on the dark web to offer “cybercrime-as-a-service.” Threat actors are selling AI-powered kits for phishing, malware obfuscation, fake documentation, and fraudulent identity creation. [MIT Technology Review, 2023]

These developments underscore the urgent need for dynamic cyber defense models that incorporate AI not just for detection, but also for predictive analytics and rapid response. Cyber insurance providers are also revising underwriting models to reflect the growing influence of AI-enabled risks.

Indian Cyber Security Insurance Industry: A Critical Assessment

The cyber insurance market in India is still in its infancy, despite a dramatic surge in cyber threats and digital vulnerabilities. While digital transformation has accelerated, insurance adoption has not kept pace, creating a wide protection gap for businesses of all sizes. Below is a comprehensive assessment of the key challenges and emerging trends shaping the Indian cyber insurance landscape:

- Underpenetration: Less than 1% of Indian enterprises currently hold cyber insurance policies—a stark contrast to developed markets like the U.S. or U.K., where adoption rates exceed 30–40% in certain sectors. This lack of adoption leaves businesses exposed to potentially devastating cyber incidents. [Economic Times, 2023]

- Rising Demand Amid Attacks: According to the Indian Computer Emergency Response Team (CERT-In), India witnessed over 1.4 million cyber incidents in 2023, spanning ransomware, phishing, and data breaches. The sheer volume of attacks is catalyzing demand for coverage—particularly among fintechs, hospitals, and ITES firms.

- Low Awareness Levels: Despite increased risk exposure, more than 60% of Indian businesses are unaware of the scope and benefits of cyber insurance, especially among MSMEs and Tier-II enterprises. This results in missed opportunities to mitigate financial and reputational risks. [Down To Earth, 2023]

- Generic & Misaligned Products: Many Indian insurers rely on reworded Western policy templates that fail to reflect the domestic legal landscape, cultural nuances, and unique threat vectors. This leads to ambiguity in claim settlements and inadequate coverage.

- Premium vs. Claim Disconnect: A growing number of policies are being issued, yet claim activity remains low. This is attributed to poor breach detection, delayed reporting, and lack of clarity about what is covered. Businesses often purchase policies for compliance rather than protection.

- Talent Deficit in Underwriting: India faces a shortage of specialized cyber underwriters and actuarial professionals who can accurately assess digital risks. This hinders product innovation and contributes to pricing inefficiencies. As of 2025, cyber-specific underwriting training programs remain limited across the insurance sector.

Overall, India’s cyber insurance industry stands at a crucial inflection point. Bridging the awareness gap, building customized products, enhancing regulatory clarity, and nurturing talent will be critical to unlocking its true potential.

Government and Regulatory Guidelines

As cyber threats become more complex and frequent, Indian regulators have taken critical steps to strengthen cyber resilience across sectors. While cyber insurance remains largely voluntary, regulatory nudges and governance frameworks are paving the way for wider adoption. Here’s an overview of the key government and regulatory developments influencing the cyber insurance landscape in India:

- IRDAI (Insurance Regulatory and Development Authority of India): India’s apex insurance regulator has consistently urged insurers to standardize cyber insurance offerings and launch awareness campaigns targeting both SMEs and large corporations. IRDAI has formed task forces to explore product innovation and reporting frameworks for cyber claims. [IRDAI Official Website]

- RBI (Reserve Bank of India): The RBI has not mandated cyber insurance, but it recommends banks and non-banking financial institutions (NBFCs) to consider it as a key component of their operational risk management under its IT Framework for NBFCs. Banks are encouraged to hedge against data breaches, fraud, and ransomware by availing cyber risk covers.

- SEBI (Securities and Exchange Board of India): SEBI mandates that listed companies adopt robust cybersecurity frameworks, particularly in financial services and trading platforms. While cyber insurance is not explicitly required, companies are expected to take all reasonable precautions to mitigate cyber risks, which includes transferring risk through insurance.

- DPDP Act (2023): The Digital Personal Data Protection Act, 2023, India’s landmark data privacy law, has significantly raised the stakes for data protection. It introduces strict obligations on data fiduciaries, including financial penalties for non-compliance and data breaches. While cyber insurance is not directly mentioned, the Act indirectly supports the adoption of cyber insurance as a risk mitigation measure for handling compliance costs and penalty exposures. [MeitY – Ministry of Electronics & IT]

Together, these regulatory measures reflect a growing institutional push toward resilience and accountability in cyber governance. While there is still no mandate for cyber insurance, the environment is steadily shifting to incentivize its adoption as a best practice.

Frequently Asked Questions (FAQ) about Cyber Insurance in India

1. What does cyber insurance cover in India?

Cyber insurance policies typically cover breach detection, incident response, system recovery, legal liabilities, regulatory fines, ransomware payments, business interruption, forensic audits, PR crisis support, and data privacy violation claims.

2. How much does cyber insurance cost in India?

Premiums for cyber insurance in India can vary widely depending on the size of the organization, industry-specific exposure, existing cybersecurity posture, and the depth of coverage selected:

• For businesses: Annual premiums may range from approximately ₹12,000 to ₹90,000 based on risk profile and coverage limits. [mitigata]

• For individuals: Cyber insurance may cost between ₹25,000 to ₹100,000 per year, depending on the insurer and policy inclusions. [mitigata]

• Comprehensive coverage (₹1 crore): Such plans could cost upwards of ₹200,000 annually, subject to underwriting. [pazcare]

Disclaimer: These figures are indicative and based on publicly available sources. Actual premiums vary based on policy type, plan inclusions, insurer underwriting norms, and cybersecurity controls in place. Salasar Services does not accept liability for the exact pricing mentioned above. For accurate quotes, consult a licensed insurance professional.

3. Who must report cyber incidents to CERT-In and in what timeframe?

As per CERT-In directives, all service providers, data centers, intermediaries, telecom firms, insurance companies, and corporates must report specified cyber incidents within six hours of detection.

4. Are SMEs in India buying cyber insurance?

Yes, adoption is growing, particularly in IT, logistics, fintech, and e-commerce. However, overall market penetration remains low due to cost concerns and limited awareness about coverage benefits.

5. Is cyber insurance mandatory in India?

No, cyber insurance is currently not mandatory in India. However, regulators like IRDAI, SEBI, and RBI recommend it as part of enterprise cyber risk mitigation strategies.

6. What are the eligibility requirements for cyber insurance?

Insurers usually require the organization to have basic cybersecurity hygiene such as firewalls, antivirus software, employee training, periodic risk audits, and data protection policies in place.

7. Does cyber insurance cover regulatory fines and penalties?

Yes, many policies cover fines or penalties from regulators like CERT-In or DPDP authorities, provided the breach was unintentional and the policyholder met compliance obligations before the incident.

8. What is the future outlook for cyber insurance in India?

India’s cyber insurance market is expected to grow at a CAGR of 25–30%, surpassing USD 100 million in premiums by 2026. [PwC India]

9. Do cyber insurance policies cover reputational damage?

Some policies include provisions for PR crisis management, customer notification, and media handling to mitigate reputational fallout post-breach. However, these are typically subject to sub-limits or optional add-ons.

10. How are cyber insurance claims settled in India?

Claims are evaluated based on policy terms, forensic reports, regulatory notices, and documentation of financial losses. Delayed or incomplete incident reporting often leads to disputes or partial settlements.

11. Does personal cyber insurance exist for individuals in India?

Yes, several insurers offer individual cyber insurance policies that protect against risks like identity theft, phishing, cyberbullying, financial fraud, and online harassment.

12. Does cyber insurance cover employee mistakes?

Yes, most policies cover incidents arising from employee negligence such as falling for phishing attacks, misconfiguring cloud settings, or accidental data exposure—provided they were not intentional acts.

13. What types of cyber insurance are available in India?

Common types include Individual Cyber Insurance, Business Cyber Insurance, Data Breach Insurance, Cyber Liability Insurance, Technology Errors & Omissions (E&O), and Cybercrime Insurance covering fraud and extortion.

14. Can cyber insurance be bundled with other business covers?

Yes, insurers often bundle cyber risk coverage with other enterprise packages like professional indemnity, directors & officers liability, or property insurance for operational convenience and premium efficiency.

AI in Risk Assessment: How Smart Technology is Redefining Business Safety

In today’s volatile business environment, decision-making backed by data is not just a strategic advantage—it’s a necessity. Artificial Intelligence (AI) is rapidly transforming how businesses assess and manage risks. From automating claims to identifying hidden exposures, AI empowers businesses to make smarter, faster, and more precise decisions in their risk management journey.

Understanding AI-Driven Risk Analysis

AI-powered risk analysis refers to the use of machine learning algorithms, data analytics, and predictive modeling to identify, evaluate, and mitigate business risks. These tools digest massive volumes of structured and unstructured data, allowing for real-time analysis and proactive risk strategies.

Unlike traditional models that rely heavily on static historical data, AI systems learn and adapt—enabling dynamic forecasting and early-warning alerts.

Why Businesses Need AI-Enhanced Risk Tools Today

- Uncertainty is the New Normal: From geopolitical shifts to climate change and cyber threats, the risk landscape is expanding.

- Data Overload: Businesses now generate enormous data from IoT, customer interactions, logistics, and operations. Manual analysis is inefficient and incomplete.

- Insurance Premium Optimization: Risk profiles powered by AI help businesses negotiate better insurance terms by showcasing improved risk postures.

Key Benefits of AI-Powered Risk Analysis

1. Real-Time Risk Monitoring

AI enables 24/7 monitoring of operational, cyber, and financial data. With automated alerts, businesses can respond immediately to anomalies and reduce losses from delayed interventions.

2. Predictive Risk Modeling

AI models assess risk probability based on historical patterns, real-time signals, and external datasets. This helps forecast supply chain disruptions, default risks, or compliance failures before they escalate.

3. Fraud Detection and Prevention

Insurers and businesses use AI to detect inconsistencies in transactions and claims. Machine learning models learn typical patterns and raise red flags for fraudulent behavior[Deloitte].

4. Tailored Insurance Solutions

Risk scoring backed by AI gives insurers more precise underwriting inputs. This allows brokers to design custom insurance programs that reflect a company’s unique operational exposures[McKinsey].

5. Cost Optimization and Operational Efficiency

AI reduces manual work, eliminates redundant data processing, and minimizes human error. Over time, this translates into lower costs and faster decision cycles.

AI and Business Insurance: A Stronger Risk Partnership

For insurance brokers and risk advisors, AI-powered analytics become indispensable in guiding clients across sectors—from manufacturing and logistics to retail and healthcare. These tools allow brokers to:

- Design risk prevention strategies that reduce claim incidence

- Back insurance negotiations with data-backed insights

- Advise clients on optimal coverage and limits

- Assist in loss forecasting and catastrophe modeling

Ultimately, this elevates the role of brokers from intermediaries to strategic risk advisors.

Examples of AI in Action

- ICICI Lombard uses AI in its mobile app to inspect car damage for instant policy renewals[Microsoft].

- Aditya Birla Health rewards insureds based on health data from wearables integrated with its Activ Health App[NDTV Profit].

Final Thoughts

AI-powered risk analysis is more than a digital transformation—it’s a competitive edge. Businesses that embrace intelligent risk systems stand to gain with faster claims processing, reduced losses, optimized insurance premiums, and sharper operational insights.

For insurers and brokers alike, it's time to evolve from traditional, reactive models to agile, AI-enhanced risk frameworks. The future of business insurance is intelligent, real-time, and data-driven.

Frequently Asked Questions (FAQ)

1. How does AI improve risk management in insurance?

AI enables predictive modeling, real-time monitoring, and fraud detection. These tools help underwriters and brokers assess risk more accurately and proactively reduce exposure. [Deloitte]

2. Can AI help reduce business insurance premiums?

Yes. Businesses with better risk profiles, backed by AI data, can often negotiate lower premiums due to improved risk mitigation and loss ratios. [McKinsey]

3. Is AI relevant for small and mid-sized businesses?

Absolutely. Scalable AI solutions are now accessible to SMEs. These tools help automate compliance, forecast supply chain disruptions, and improve cyber risk detection. [Harvard Business Review]

4. Can AI help predict cyber risks before an attack occurs?

Yes. AI-powered risk tools can analyze security logs, threat intelligence, network activity, and behavioral patterns to identify warning signs before incidents escalate. For businesses, this can support earlier intervention, stronger cyber controls, and better insurance risk documentation. [IBM]

5. What industries benefit the most from AI-powered risk analysis?

Industries with complex, data-heavy risk environments benefit the most, including insurance, banking and financial services, healthcare, manufacturing, logistics, retail, and e-commerce. These sectors generate large volumes of operational, financial, customer, and claims data, making AI useful for identifying anomalies, emerging exposures, and risk trends. [McKinsey]

6. Can AI improve insurance claims processing?

Yes. AI can help automate claim intake, document review, image assessment, fraud flagging, and workflow routing. This can reduce processing time, improve consistency, and allow claims teams to focus on complex cases that require human judgment. [Deloitte]

7. What are the limitations of AI in risk management?

AI is powerful, but it is not foolproof. Its effectiveness depends on data quality, model design, governance, and human oversight. Poor data, algorithmic bias, lack of transparency, privacy concerns, or overreliance on automated outputs can lead to flawed risk decisions. Businesses should treat AI as a decision-support tool, not a substitute for expert risk judgment. [World Economic Forum]

8. Is AI-powered risk analysis expensive to implement?

Not always. Large enterprises may invest in advanced custom AI systems, but smaller businesses can start with cloud-based analytics, cyber monitoring platforms, SaaS tools, or insurer-supported risk dashboards. The cost depends on data complexity, integrations, compliance needs, and the level of automation required. [Harvard Business Review]

9. Will AI replace human risk managers and insurance professionals?

No. AI is more likely to augment risk and insurance professionals than replace them outright. It can process large datasets, identify patterns, and automate repetitive tasks, but human expertise remains essential for interpreting context, advising clients, negotiating coverage, managing compliance, and making judgment-based decisions. [World Economic Forum]

The Importance of Business Insurance for SMEs: A Lifeline for Growth and Stability

In the dynamic world of small and medium-sized enterprises (SMEs), entrepreneurs often wear multiple hats—managing operations, finances, marketing, and more. Amidst the hustle, one critical aspect that frequently gets overlooked is business insurance. While it may seem like an unnecessary expense, especially for businesses operating on tight budgets, the reality is that business insurance is not just a safety net—it’s a strategic tool for growth and stability. Let’s delve into why SMEs must prioritise business insurance and how it can be a game-changer in navigating risks and ensuring long-term success.

Understanding the Risks SMEs Face

SMEs are the backbone of any economy, contributing significantly to employment and innovation. However, their size and resource constraints make them particularly vulnerable to risks. Unlike large corporations, SMEs often lack the financial cushion to absorb unexpected losses. A single unforeseen event—be it a natural disaster, a lawsuit, or a cyberattack—can cripple operations and, in some cases, force the business to shut down permanently. For instance, consider a small bakery serving its community for years. A fire breaks out due to an electrical fault, destroying the kitchen equipment and inventory. Without insurance, the cost of rebuilding and replacing assets could be insurmountable. The bakery, which was once a thriving business, might never recover. This is where business insurance steps in. It acts as a financial shield, protecting SMEs from the unpredictable and ensuring they can bounce back from setbacks.Top Risks Faced by SMEs

Protection Against Property Damage

For many SMEs, their physical assets—such as equipment, inventory, and office space—are the foundation of their operations. Property insurance covers damages caused by events like fires, floods, or theft. This means that if disaster strikes, the business can recover without bearing the full financial burden. Take the example of a small manufacturing unit. A flood damages machinery worth lakhs of rupees. With property insurance, the owner can claim the cost of repairs or replacements, ensuring minimal disruption to operations.Liability Coverage: Shielding Against Legal Risks

In today’s litigious environment, lawsuits can arise from unexpected quarters. A customer might slip and fall in your store, or a client could claim negligence in your services. Liability insurance covers legal fees, settlements, and medical expenses, protecting your business from potentially devastating financial losses. Imagine a scenario where a customer alleges food poisoning from a meal at your restaurant. Without liability coverage, the legal costs alone could drain your resources, even if the claim is unfounded.Business Interruption Insurance: Keeping the Lights On

Disasters don’t just damage property—they can also disrupt operations. Business interruption insurance compensates for lost income during downtime, helping you pay rent, salaries, and other expenses while you get back on your feet. For example, a tech startup faces a cyberattack that halts operations for weeks. With business interruption insurance, the company can cover its fixed costs and retain employees, even when revenue streams are temporarily cut off.Employee Protection: Building Trust and Loyalty

Employees are the lifeblood of any business. Insurance policies like workers’ compensation and group health insurance not only protect your team but also enhance employee satisfaction and retention. When employees feel secure, they are more likely to be productive and committed to the company’s success. Consider a small construction firm where a worker gets injured on the job. Workers’ compensation ensures the employee receives medical care and financial support, while the employer avoids costly legal battles.Tailored Insurance Strategies: One Size Doesn’t Fit All

One of the most common mistakes SMEs make is opting for generic insurance policies. Every business is unique, with its own set of risks and challenges. A one-size-fits-all approach often leaves critical gaps in coverage, leaving businesses vulnerable. For instance, a software development company faces cyber risks that a retail store might not. Similarly, a logistics company needs coverage for its fleet of vehicles, which is irrelevant for a consultancy firm. Tailored insurance strategies ensure that your policy aligns with your specific needs, providing comprehensive protection.Real-Life Example: The Power of Customized Insurance

Let’s look at the case of a mid-sized e-commerce business. The company initially opted for a standard insurance package, only to realize it didn’t cover cyber risks. When a data breach exposed customer information, the business faced hefty fines and a loss of customer trust. After this incident, the company worked with an insurance expert to design a customized policy that included cyber liability coverage. The next time a breach occurred, the insurance covered the costs, allowing the business to recover quickly and maintain its reputation.Building Trust with Clients and Investors

Business insurance isn’t just about risk management—it’s also a credibility booster. Clients and investors are more likely to trust and engage with a business that demonstrates foresight and responsibility. For instance, a construction company with comprehensive insurance is more likely to win contracts, as clients feel assured that any mishaps will be managed professionally.Overcoming the Cost Barrier

Many SMEs hesitate to invest in insurance due to cost concerns. However, the expense of a policy pales in comparison to the potential losses from an uninsured event. Moreover, insurance premiums can often be tailored to fit your budget, and the peace of mind it provides is invaluable.Steps to Choose the Right Insurance

- Assess Your Risks: Identify the specific risks your business faces. For example, a restaurant might prioritize fire and liability coverage, while a tech firm might focus on cyber risks.

- Consult an Expert: Work with an insurance advisor to design a policy that meets your unique needs.

- Compare Policies: Don’t settle for the first option. Compare different policies to find the best coverage at a reasonable cost.

- Review Regularly: As your business grows and evolves, so do its risks. Regularly review and update your insurance policy to ensure it remains relevant.

Conclusion: Insurance as a Growth Enabler

Business insurance is often viewed as a defensive measure, but it’s much more than that. For SMEs, it’s a strategic investment that safeguards their present and secures their future. By mitigating risks, building trust, and ensuring continuity, insurance empowers SMEs to focus on what they do best—growing their business. In a world full of uncertainties, business insurance is the one certainty SMEs can rely on. Don’t wait for disaster to strike. Take the proactive step today and protect your business, your employees, and your dreams. After all, a secure business is a successful business.

Health Insurance Claim Rejections: Tips to Avoid Rejections & How Brokers Can Assist

Health insurance is meant to be a safety net, a financial cushion that protects you during medical emergencies. But what happens when that safety net fails? Imagine this: You’ve just undergone surgery, and you’re already stressed about recovery. Then, you receive a letter from your insurance company—your claim has been rejected. Sounds like a nightmare, right? Unfortunately, this scenario is all too common. According to a recent study, nearly 50% of health insurance policyholders faced full or partial claim rejections in the last three years*. That’s half of the people who trusted their insurance to cover their medical expenses, only to be left in the lurch. Why does this happen? More importantly, how can you prevent it? And what role can insurance brokers play in ensuring your claims are approved? Let’s dive in. Why Are Health Insurance Claims Rejected? Claim rejections can feel like a slap in the face, especially when you’re already dealing with health issues. But understanding the reasons behind these rejections can help you avoid them. Here are the most common culprits: 1. Non-Disclosure of Pre-Existing Diseases One of the biggest reasons for claim rejections is the failure to disclose pre-existing conditions. Let’s say you have diabetes but didn’t mention it when buying the policy. Later, if you file a claim related to diabetes, the insurer can reject it, citing non-disclosure. Example: Ramesh, a 45-year-old businessman, had high blood pressure but didn’t disclose it while purchasing his policy. When he filed a claim for a heart-related surgery, it was rejected because the insurer found out about his pre-existing condition during verification. 2. Policy Exclusions Every health insurance policy has exclusions—specific conditions or treatments that aren’t covered. Many policyholders don’t read the fine print and are shocked when their claims are rejected. Example: Cosmetic surgeries, maternity treatments, and alternative therapies like Ayurveda are often excluded. If you undergo a procedure that falls under these categories, don’t expect your insurer to cover it. 3. Incorrect or Incomplete Documentation Insurance companies are sticklers for paperwork. Missing or incorrect documents can lead to claim rejections, even if your treatment is covered. Example: Geeta forgot to submit her discharge summary and prescription bills while filing a claim for her knee surgery. Her claim was rejected due to incomplete documentation. 4. Waiting Period Violations Most health insurance policies have waiting periods for specific treatments or pre-existing conditions. If you file a claim before the waiting period is over, it will likely be rejected. Example: A policy might have a 2-year waiting period for cataract surgery. If you undergo the surgery within 18 months, your claim won’t be approved. 5. Treatment at a Non-Network Hospital Many policies require you to get treated at network hospitals to avail of cashless facilities. If you choose a non-network hospital, your claim might be rejected or only partially approved. Example: Priya opted for a non-network hospital because it was closer to her home. While her treatment was covered, her claim was rejected because the hospital wasn’t part of the insurer’s network. How to Prevent Health Insurance Claim Rejections Now that we know the reasons, let’s talk about how to avoid these pitfalls. Here are some practical steps you can take: 1. Be Honest About Your Medical History When buying a policy, disclose all pre-existing conditions, no matter how minor they seem. This ensures there are no surprises later. Tip: Keep all your medical records handy while filling out the application form. 2. Read the Policy Document Thoroughly Yes, policy documents can be tedious, but they’re essential. Pay special attention to the exclusions, waiting periods, and network hospital list. Tip: If you don’t understand something, ask your insurer or broker for clarification. 3. Double-Check Your Documents Before submitting a claim, ensure all required documents are in order. This includes bills, prescriptions, discharge summaries, and diagnostic reports. Tip: Create a checklist of documents required for claims and tick them off as you go. 4. Be Aware of Waiting Periods Know the waiting periods for specific treatments and pre-existing conditions. Plan your treatments accordingly to avoid claim rejections. Tip: If you’re unsure about waiting periods, consult your insurer or broker. 5. Choose Network Hospitals Whenever possible, opt for network hospitals to avail of cashless facilities. If you must go to a non-network hospital, inform your insurer beforehand. Tip: Keep a list of network hospitals handy, especially if you travel frequently. What Can Insurance Brokers Do to Help? Insurance brokers aren’t just middlemen; they’re your allies in navigating the complex world of health insurance. Here’s how they can help: 1. Help You Choose the Right Policy Brokers have in-depth knowledge of various policies and can recommend one that suits your needs and budget. Example: A broker helped Sunita, a 60-year-old retiree, find a policy with comprehensive coverage for her pre-existing conditions at an affordable premium. 2. Explain Policy Terms in Simple Language Brokers can break down complex policy terms and conditions, ensuring you understand what’s covered and what’s not. Example: Ravi, a first-time policyholder, was confused about co-payment clauses. His broker explained it to him in simple terms, helping him make an informed decision. 3. Assist with Documentation Brokers can guide you on the documents required for claims and even help you fill out forms correctly. Example: When Anjali’s father was hospitalized, her broker helped her gather and submit all the necessary documents, ensuring a smooth claims process. 4. Appeal Rejected Claims If your claim is rejected, brokers can help you file an appeal. They know the ins and outs of the process and can increase your chances of success. Example: After Rajesh’s claim was rejected due to a technical error, his broker helped him file an appeal with the correct documents, and the claim was eventually approved. Real-Life Example: How a Broker Saved the Day Let’s look at a real-life scenario. Meena, a 50-year-old teacher, was diagnosed with breast cancer. She had a health insurance policy but wasn’t aware of the waiting period for cancer treatments. When she filed a claim, it was rejected because the waiting period wasn’t over. Feeling helpless, Meena approached her insurance broker. The broker reviewed her policy and found that while the waiting period for cancer treatments was two years, Meena had completed one year and ten months. The broker advised her to wait two more months before undergoing treatment. Meena followed the advice, and her claim was approved without any issues. This example highlights the importance of having a knowledgeable broker by your side. Conclusion: Be Proactive, Stay Informed Health insurance claim rejections can be frustrating, but they’re often avoidable. By being honest about your medical history, reading the fine print, and keeping your documents in order, you can significantly reduce the chances of rejection. And remember, you don’t have to navigate this journey alone. Insurance brokers are there to guide you, from choosing the right policy to filing claims and appealing rejections. With the right knowledge and support, you can ensure that your health insurance truly serves as a safety net when you need it most. So, take charge of your health insurance today. After all, peace of mind is priceless. *https://www.moneycontrol.com/news/business/personal-finance/nearly-half-of-health-insurance-policyholders-faced-full-or-partial-claim-rejection-in-last-three-years-study-12902484.htm

Key Points To Consider Before Choosing An Insurance Plan

Selecting the appropriate insurance plan is a crucial financial choice that you will face in your lifetime. It is essential for safeguarding your family, health, and assets, ensuring you are equipped for life's uncertainties. Understanding the intricacies of choosing the right insurance plan is vital. In India, insurance brokers offer specialised solutions at optimised costs across various sectors and industries. Their primary aim is to simplify the decision-making process, making it more informed and accessible for you.

Why is Choosing the Right Insurance Plan Important?

An insurance plan serves as a financial safety net, providing you with peace of mind in times of need. The right insurance plan can help cover medical expenses, secure your family’s future, protect your assets, and even provide tax benefits. However, with the plethora of insurance plans available in the market, choosing the right one can be overwhelming. This is where understanding the key points to consider before choosing an insurance plan becomes crucial. Key Points to Consider Before Choosing an Insurance Plan 1. Assess Your Needs Before you start looking for an insurance plan, it’s important to assess your specific needs. Ask yourself questions like:- What am I trying to protect?

- How much coverage do I need?

- What is my budget?

- Life Insurance Plan: This provides financial support to your family in case of your untimely demise.

- Health Insurance Plan: Covers medical expenses incurred due to illnesses or injuries.

- Motor Insurance Plan: Protects against damages to your vehicle and third-party liabilities.

- Home Insurance Plan: Covers damages to your home and its contents.

- Travel Insurance Plan: Provides coverage for travel-related issues such as trip cancellations, lost baggage, and medical emergencies abroad.

- Coverage: Ensure that the plan covers all your needs.

- Premiums: Compare the premiums of different plans to find one that fits your budget.

- Exclusions: Check what is not covered by the plan.

- Claim Process: Understand the claim process and the time taken to settle claims.

- Coverage Limitations: Know the maximum amount the policy will pay.

- Deductibles: The amount you need to pay out of pocket before the insurance kicks in.

- Waiting Periods: The time you need to wait before certain coverages become effective.

- Renewability: Check if the policy can be renewed and under what conditions.

- Critical Illness Rider: Provides additional coverage in case you are diagnosed with a critical illness.

- Accidental Death Benefit Rider: Offers additional payout in case of accidental death.

- Waiver of Premium Rider: Waives off future premiums if you become disabled and unable to work.

Common Mistakes in Property Claims Management and How to Avoid Them?

Property claims management can be a complex and daunting process, often fraught with potential pitfalls. Properly managing these claims is crucial to ensuring that you receive the coverage you need in times of crisis. At Salasar, we are dedicated to making insurance decisions easier and more informed. With specialised solutions at optimised costs across verticals and industries, our team ensures you always have the right coverage.

Here are some common mistakes in property claims management and how to avoid them.

1. Not Understanding Your Policy:

A common mistake in property claims management is not thoroughly understanding your insurance policy. Many policyholders overlook the fine print, which can lead to unexpected issues when filing a claim. Your policy includes essential details about coverage limits, exclusions, and conditions that must be met for a claim to be accepted. Neglecting to familiarise yourself with these aspects can result in denied claims or inadequate compensation. To avoid this, take the time to read and understand your policy thoroughly, ensuring you are aware of what is covered and any potential limitations. How to Avoid It: Thoroughly read your policy and ask your insurance broker for clarification on any points you don’t understand. We offers personalised consultations to help you comprehend every aspect of your coverage, ensuring there are no ambiguities.2. Delaying the Claim Filing:

Filing a claim promptly is crucial. Delays can result in complications or even denial of your claim. Insurance companies set specific deadlines for reporting claims, and missing these deadlines can jeopardise your ability to receive compensation. Therefore, it is vital to report any incidents as soon as possible to ensure your claim is processed smoothly. Always be aware of your insurer's time frames and act quickly to avoid any unnecessary issues. We help you navigate these timelines efficiently, ensuring you meet all requirements for a successful claim. How to Avoid It: File your claim as soon as the incident occurs. Keep all necessary documents and evidence ready to expedite the process. Our team assists you in gathering and organising all required documentation swiftly and efficiently.3. Inadequate Documentation:

Lack of proper documentation can significantly impede your claims process. Without sufficient evidence of the damage or loss, your claim may be delayed, reduced, or even denied. Comprehensive records, including photographs, receipts, and detailed inventories, are essential to support your claim. It's crucial to document everything meticulously at the time of the incident to ensure a smooth and successful claims process. This proactive approach helps provide the necessary proof to the insurance company, facilitating a fair and timely settlement. We emphasise the importance of thorough documentation to help you navigate property claims management effectively. How to Avoid It: Document everything meticulously. Take photographs, maintain receipts, and record detailed descriptions of the damage. Our experts can guide you on the essential documents and evidence needed to support your claim effectively.4. Overlooking Policy Exclusions: